[Edit: this post was written before President Trump announced his tariffs on 4/2. Still think a compelling setup for those with multi-year duration, but this may introduce a material headwind to near-term ticket sale estimates.]

That was a surprising reaction to an above-expectations Q4 ’24 earnings print.

But then again, the company didn’t settle the MSGN debt issue, didn’t sign the official Abu Dhabi contract after announcing in October, and didn’t take the $30m/yr naming sponsorship deal. The venue is still ramping and won’t see revenue acceleration until Q2 ’25. A lot of missed catalysts for catalyst-driven traders in the stock.

I still think Sphere works.

I would analogize Sphere today to launching Disneyland with only 60% of rides operational. The true unit economics will only be seen when operating at full capacity. And the economics dramatically improve with each new Disneyland campus.

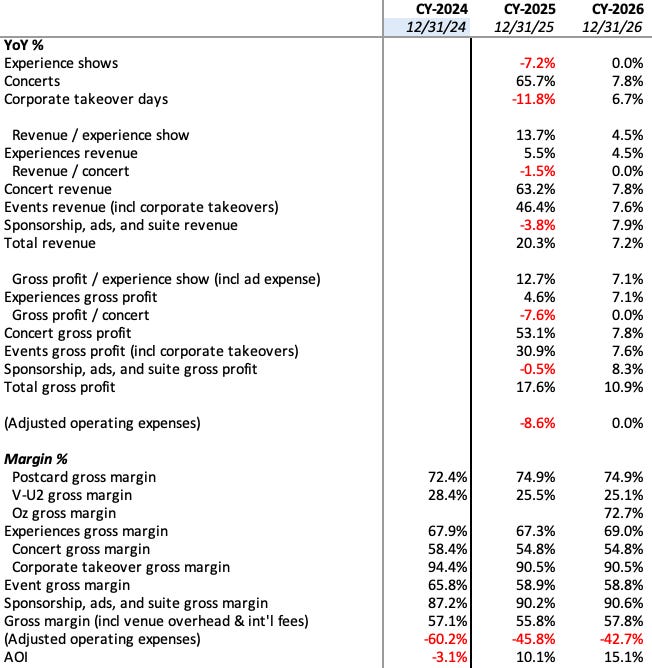

Sphere will accelerate revenue with improving operating margins in 2025 for 3 reasons:

1. Replacing the weak V-U2 show with Oz (purple)

2. Increasing concert count by >65% YoY (green)

3. Reducing SG&A to $100m/q (yellow)

First, V-U2 (purple) is an underperforming recorded concert film that is weighing on gross margin. Hard to say exactly why it’s not attracting crowds. My take is that it’s stuck between a true concert and a sit-down movie. The content is well-shot, and the sound system is amazing, but a concert feels low energy if 90% of the audience is treating it like a documentary. V-U2 also launched with only 2 weeks of pre-marketing, so it never had an initial buzz. I estimate revenue/show is ~50% of Postcard at a 25%-30% gross margin after U2’s cut.

Once Oz launches on July 1, Sphere will see an immediate boost. If Oz sells at the same pace as Postcard, Oz should earn ~3x gross profit per show compared to V-U2. Oz pre-marketing will begin in March, which should give plenty of time to build awareness for the July launch.

Second, Sphere is on track for a 120+ concert runrate (green). Bands are selling far more tickets than expected: Kenny Chesney has sold ~250k and Backstreet Boys ~300k. This revenue is effectively pre-booked, which locks in accelerating revenue growth. No other venue sells tickets at this pace. Sphere’s first year earned the highest annual gross for any venue of any size in Boxscore history - and that was with a low concert count.

I estimate concert count grows >65% YoY from 70 in 2024 to 116 in 2025: from today’s calendar, add 1 more BSB weekend + 35 Harry Styles + another 5 day EDM New Year’s Eve run.

Starting in May 2025, every concert week is averaging at least 3 shows. We already see 31 concerts in CQ2 ’25. At this pace, 2026 should reach 125 concerts.

(Update: NY Post was apparently incorrect about Harry Styles coming to Sphere. We’ll find out in ~ May/June about the H2 ‘25 performers.)

Note that the sellside won’t update from the company’s sandbagged guidance until concerts are announced – so consensus estimates will be artificially low, setting up a natural beat and raise cadence.

Third, Sphere has walked down SG&A estimates (yellow) from $105m/q ex one-offs to ~$100m/q. The Las Vegas venue is moderately overstaffed, and most SG&A is non-venue corporate overhead, so they could cut further if desired.

With fewer V-U2 shows, Oz performing in-line with Postcard, and more concerts, Sphere should accelerate to ~50% revenue growth in Q3 ’25 and >20% for CY ‘25. Gross margin will improve with Oz replacing V-U2. Operating margin will further improve as Sphere embarks on a Year of Efficiency.

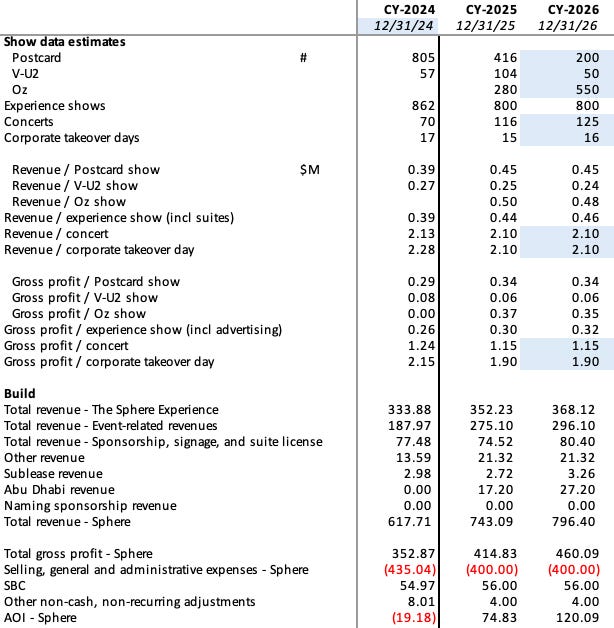

Flowing this through to 2026 implies that $35.40/sh = ‘26e ~13.5x EV/AOI and ~8.5x AOI after Abu Dhabi launches (2028?).

This valuation excludes upside from naming rights or improved ad sales or new Experiences, penalizes cash $100m for MSGN, assumes SPHR sells the London land at cost, and ignores dilution >$75/sh. It also excludes new Spheres. And if Sphere Abu Dhabi works, do you think other cities will want one?

SPHR should be a 2x in 3y from a model only ~60% into its launch…

(Revenue per Experience show modeled at Q1 ’25 estimated runrate; assume new 2026 Experiences at similar pace)

…and Sphere should reach “fully launched” in 2026.

Here’s what I think Sphere looks like at maturity:

-At least 3 films in rotation (Postcard, Oz, ?)

-At least 3 recorded concerts that actually sell (i.e. drawing a 6k-10k crowd on non-concert weekends). V-U2 in its present form doesn’t count. EDM is what we should expect.

-130+ concerts (MSG hosts live events 4-5 days/week, so this feels like a reasonable maximum for Sphere)

-$10+m of sponsorship sales for venue areas (remembering for context that Dolan turned down a $30m naming sponsorship; note that MSG has had Chase entrances, Chase lounge, Motorola VIP seating, Anheuser-Busch Blue Seats, etc).

-Consistent Exosphere ad sales

-Winning deals to build Spheres 3/4/5

All of the above is material upside to our current model.

So at today’s immature performance level, you get SPHR at a low FY1 valuation and a downright cheap valuation on the 4y out Abu Dhabi runrate.

Sphere is poised to drive more concert volume and better Experiences from here.

And Sphere is exploring new form factors to attract more franchisees (eg smaller venues, perhaps a diminished Exosphere if the city doesn’t want bright outdoor images at night).

Each new Sphere is worth an incremental $27/sh-$36/sh ($75m-$100m AOI * 18x fwd multiple) if as large as Abu Dhabi – or $15-20/sh if smaller. Put differently, one more Abu Dhabi-sized Sphere deal would be worth today’s entire market cap.

MSGN debt clearance will be a nice boost, but likely <$5/sh impact.

Q1 ’25 will continue to look flattish YoY as V-U2 drags on performance.

Starting Q2 ’25, the acceleration will print, and the stock should reprice.

Risks of note

Sphere’s disclosures are too opaque.

Not a business risk, but a stock risk.

Analysts won’t properly model Sphere’s earnings power without more clarity on venue-level profitability.

The Las Vegas venue AOI (excluding corporate overhead) will approach $300m in 2025 @ 40% of total SG&A. The venue may be even more profitable if operating expenses are as low as noted in the old Las Vegas GM job posting:

Sphere brings an incremental ~1.5m tourists to Las Vegas each year. For that estimate: 115 concerts * 16.5k/concert * ~80% assumed only visiting Las Vegas for the Sphere concert.

Once you see the venue AOI and the tourist numbers, it’s a lot easier to believe other cities would want a Sphere.

Disclosing Abu Dhabi economics in detail would help here too.

Oz’s performance is difficult to predict.

In a mature model with multiple pieces of content in rotation, Sphere won’t be that sensitive to a single film launch.

But for near term downside modeling, assume Oz’s opening quarters are ~80% of Postcard’s opening ticket sales per show. Sphere would still be trading ‘26e ~16x EV/AOI and ~11.5x AOI runrate with Abu Dhabi. I think that’s still far too cheap.

Some films will inevitably outperform others – and the larger the library, the easier it is to get comfortable with runrate ticket sales. Investors should underwrite the normalized runrate as the venue matures.

Concerts may take longer to ramp to 120/yr runrate.

If you check the Sphere events calendar, you’ll see that every concert week from May through August is averaging 3 shows. For a 13 week quarter, 10 3-concert weeks + 1 extra concert gets you to ~125 concerts/yr. Any industry check will tell you that there is no shortage of artist demand. It’s possible in the near term that Sphere hasn’t nailed down this scheduling for a few weeks in H2 ’25, which would mean we’re off by a few concerts in CY ‘25 modeling.

Abu Dhabi’s construction timeline could take longer than we’d like to see.

Sphere Las Vegas broke ground in September 2018 and opened in September 2023. It has a 17,600 seating capacity, though the band stage makes it more like 16,500. Construction was interrupted by covid restrictions and 18 months of supply chain shortages. 5 years would be a long time to wait for Sphere 2.

For context on recent similar projects:

-Arena MRC, 46k capacity, 3 years

-Co-op Live, 23.5k capacity, ~2.5 years

-Everton Stadium, 53k capacity, ~3.4 years to opening (~3 to build)

-Jakarta International Stadium, 82k capacity, ~2.7 years

-Narenda Modi Stadium, 132k, 3.1 years

-T-Mobile Arena, 20k capacity, <2 years

-UBS Arena, 19k capacity, ~2.2 years

And for a recent UAE project including LEDs:

-Burj Khalifa (tallest building in world), ~6 years

Sphere Las Vegas was originally slated to break ground in late 2018 and open in late 2020 (~2 years).

2.5 years seems like a feasible timeframe to build Sphere Abu Dhabi, where labor is cheap and regulations are less cumbersome.

If they break ground in Summer 2025, the venue should open in January 2028. A reasonable downside case would add an extra year. Of note, Abu Dhabi’s Tourism Strategy 2030 aims to boost tourism by 2030, not launch in 2030.

Because Sphere will already have a full content library to show, Sphere Abu Dhabi should operate at a mature runrate in its opening year.

Rough math on Sphere contribution here: If Sphere Abu Dhabi earns $450m in revenue (2/3 of Las Vegas ‘25e revenue) with $150m in cash operating expenses, there would be ~$300m venue-level AOI. A $100m AOI contribution to Sphere would be 1/3 of this. In practice, this probably comes from a $50m base fee + $10m in operations consulting + $40m content licensing fee for Experiences films. This rough estimate is where Sphere guided sellside commentary, with upside above $100m contribution if Sphere Abu Dhabi outperforms.

MSG Networks debt may be non-recourse to Sphere parent but may still resolve unfavorably.

MSG Networks (“MSGN”) is Sphere’s subsidiary that runs a regional sports network (“RSN”). RSNs have struggled due to rising content costs from sports teams and waning consumer interest. In this case, MSG Sports (“MSGS”) is the main content provider and also in the Dolan universe. Altice, one of MSGN’s three major broadcast partners, blacked out MSGN before reaching a new agreement at 80% of its previous contract level. Costs up, revenue down, typical signs of a challenged model.

MSGN defaulted on an ~$800m term loan in October 2024 and entered forbearance to renegotiate. This debt is non-recourse to Sphere parent. Sphere initially signaled willingness to provide modest financial support but is prepared to let MSGN enter Ch. 11 at the end of March if no resolution is found. The MSGN term loan was quoted at $0.05 x $0.35 bid / ask in November 2024.

If creditors had a viable argument to make the loan fully recourse to Sphere parent, they would have asserted it by now instead of repeatedly extending forbearance. I’m modeling a $100m cash contribution (~$2/diluted sh) from Sphere parent to save MSGN.

If MSGN does file Ch. 11, I expect the MSGN creditor committee to explore every legal avenue to hassle Sphere parent. Some legal technicalities on related party transactions with shared corporate expenses (MSG companies use the same back office in NY), fraudulent conveyance claims, technicalities on past spinoffs, etc.

An annoyance but nothing thesis breaking.

Misalignment concerns / “The Dolans will take advantage of public investors.”

We’re always in a minority position as non-activist public investors – and that’s especially true when a family controls the supermajority voting stake.

In this instance, Jim Dolan has taken 4m SPHR shares in 3 grants since 2023 (1 2 3). 2.7m of these shares vest 25% each at $75/sh, $100/sh, $125/sh, $150/sh:

Dolan’s Sphere payouts dwarf his interests in MSGE and MSGS according to the proxies.

With the stock at ~$35/sh, we’re all aligned for the investment to rerate.

All dates mentioned are calendar year, not fiscal year.

Disclaimer: this is not financial advice or an offer of any kind. Do your own diligence. Any risk you take is your own, and we do not warrant the accuracy of anything written here. Assume we are invested in any securities mentioned & may make trading decisions without updating this note.

Please feel free to reach out here or on X @parisanalyst.